$SLNH more than a Bitcoin miner

Making green energy reliable with Cloud Computing

The Pitch

A full service mechanical technology firm starts a new company to build a wind farm in Morocco, monetized by Bitcoin, then decides to sell their old business and go all in on monetizing the grid with Bitcoin and Cloud Computing. The leadership team of the company is easily the most transparent I’ve ever seen, giving monthly updates on a per project basis and they consistently over deliver on their longer term projections. The company is bringing stability and predictability to the grid (and increasing profit margins of green energy producers) by monetizing it through computing. Energy curtailment and stranded energy are effectively things of the past. Assuming Bitcoin averages ~$40,000 this year and the network mining difficulty increases by 70% or less in 2022, at a share price of $10.80 SLNH currently trades for a forward PE of <2.

The Risks

30% of SLNH is owned by private equity firm Brookestone Partners. 7.3% of the shares are owned by DOMO Capital Management. The current marketcap is <$150m and has incredibly low trading volume with large bid/ask spreads. I am used to investing in smallcaps where low liquidity is the norm. But for anyone who’s used to investing in tech, this is probably very much not what you’re accustomed to. If you’re not used to low trading volume and low liquidity, prepare to see the stock price jump up or down 1% on a single buy/sell order. Proceed with caution.

The sale of SLNH’s legacy mechanical instruments business is neither completed, nor the terms of the sale yet disclosed.

The price of Bitcoin is falling off a cliff and is increasingly correlated with speculative tech assets like the ARK Innovation ETF, making any Bitcoin related securities a spooky place to be if the Fed follows through with their stated plan to end QE and start raising interest rates several times this year.

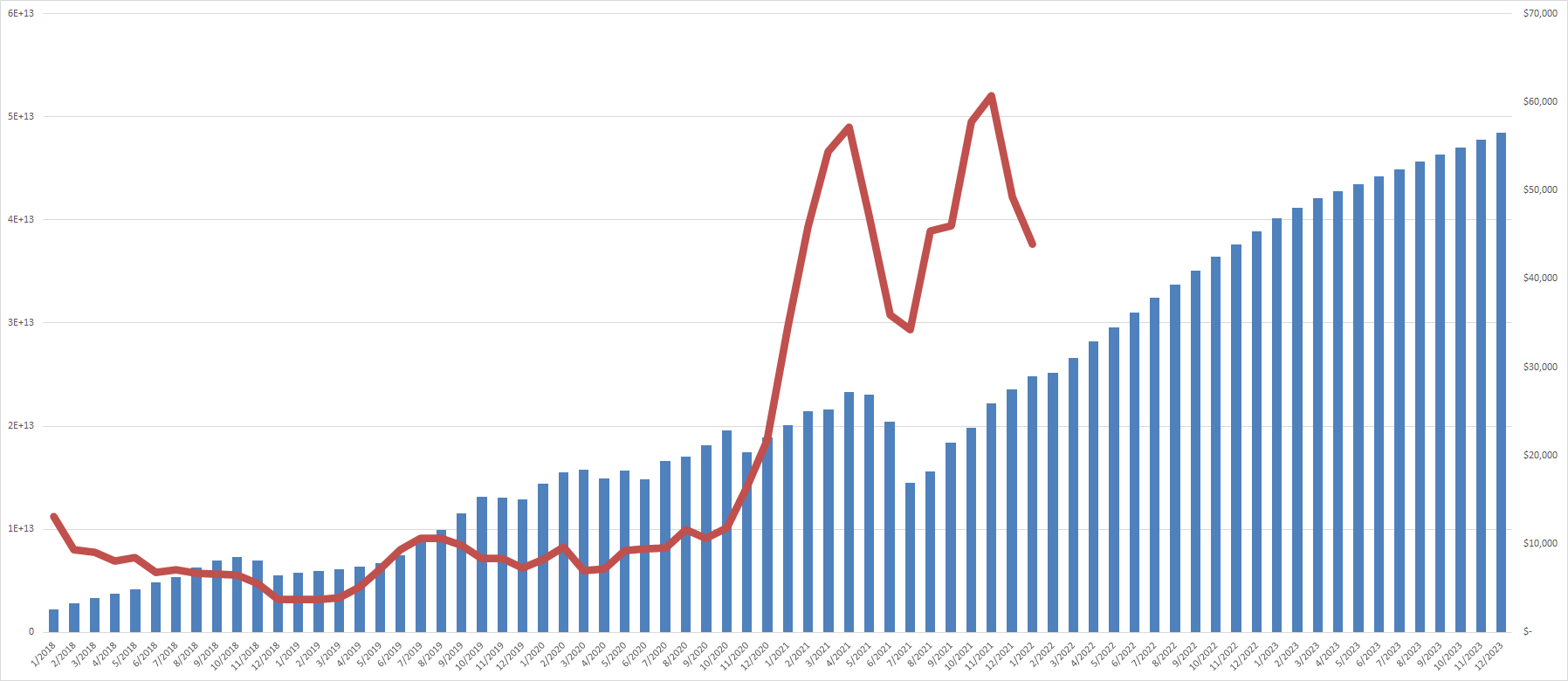

BTCUSD correlation with ARKK Assuming that other publicly traded Bitcoin miner’s current future hashrate projections are accurate, the Bitcoin network hashrate will go up at least 50% this year, putting a hard cap on the company’s margins.

SLNH’s plans for financing their upcoming projects, and achieving their stated target of 233MW of Bitcoin mining infrastructure energized and operational by the end of 2022, remain unknown.

The company does not have a common shareholder returns program.

Almost every publicly traded Bitcoin mining company has engaged in significant share dilution over the last 2 years.

Dilution to finance new Bitcoin mining equipment is a common strategy

The Upside

Unlike most of the publicly traded Bitcoin companies, SLNH isn’t speculating on the future price of Bitcoin. They’re not buying Bitcoin with their cash, they’re not ‘hodling’ the Bitcoin they mine (everything they mine is converted into cash daily), and their energy costs are the lowest in the business at under 2.5 cents/kwH. They only consider future projects which keep their cost of power below this threshold, ensuring they remain profitable in environments where other cryptocurrency mining companies can’t.

SLNH isn’t an all-in Bitcoin bet. Bitcoin could fall another 50% from here and SLNH would still be incredibly profitable and continue to execute on their long term plans. Instead of building out huge static Bitcoin mining farms, they’re effectively pitching their mining equipment as a product to green energy producers (wind, solar, hydro, geothermal). Yes, they’re pitching energy producers the right to have SLNH’s equipment operating on their sites as a service. This is why their cost of energy is able to remain so low: they are providing a service for both energy producers and for computing consumers. By providing computing consumption as a better battery for the grid (allowing energy producers to continue selling their power to SLNH when normal power demand is low, eliminating energy curtailment) while simultaneously monetizing that computing using Bitcoin for now. The company’s long term vision is to build a distributed off-grid cloud computing network. That will always include Bitcoin mining, but in the future it will also include other compute heavy tasks like Machine Learning, AI, and Scientific Computing.

Because the company isn’t singularly concerned with getting as much Bitcoin mining hashpower online as soon as possible, they are much less likely to use serial common share dilution to raise capital compared to other publicly traded Bitcoin miners. They already raised just under $16m through dilution as part of their merger last year and although I think another dilution this year is more likely than not (I’m assuming they will choose the easiest way to raise capital unless and until they publicly show another way to achieve their goals without dilution) I also think that this will be the last time the dilution lever is pulled for the foreseeable future. Bitcoin mining revenue alone will soon provide more than enough cash to finance future projects.

As part of Mechanical Technology’s recent merger with Soluna Computing, they sold off their assets with more significant geopolitical risks in Morocco. The company’s remaining assets are now de-risked.

I expect the sale of the firm’s legacy instruments business to be significantly accretive to shareholders, providing the company with significant capital that can immediately be used for their future projects, especially after receiving a $9 million USAF contract.

The leadership team’s communication is phenomenal. Monthly updates directly from the Soluna Holdings CEO, Michael Toporek, with revenue and cost breakdowns on a per project basis, in addition to regular company projections and updates to both their 6-12 month plans and projected earnings potential. In the retail space I had to wait 6 months for leadership teams to even mention they were experiencing delays on anything due to supply chain bottlenecks, and sometimes that’s all the attention it would get, a brief mention on an earnings call. SLNH was early to talking about supply chain problems, they didn’t beat around the bush about what was likely to get delayed and by how long, and they shared their efforts to prevent it from being a problem in the future. This team has consistently over delivered on their timelines and projected profit margins. For their most recent project, they literally set up a camera and let everyone watch them build it out in real time. The Soluna Computing team has their own podcast where they explain their business at length and the CEO, John Belizaire, hasn’t shied away from answering questions on other’s podcasts either. I wouldn’t blink paying a premium for this level of transparency, and I can only dream of this kind of regular communication from the leadership of names in the commodity and energy space that I’m used to owning. (Imagine not having to model AMR or DAC, or having to guess about their contracts or 6 month plans, and instead having all of their updated numbers each month broken down for you per site/ship by the CEO… 🤤)

This is an exponential growth story. As of December 9th, SLNH had around 50MW of mining equipment currently energized and operational. They plan to have 100MW up and running by the end of Q2 2022, 233MW operational and energized by the end of 2022, and a 700MW pipeline of future projects by the end of the year as well. That brings their expected Bitcoin hashrate over 4 exahash by the end of 2022.

SLNHP (the company’s non-convertible Preferred shares) have a yield of 9% and are currently trading at a steep discount to their $25 par. At $19/share they have a present annual yield over 11.8%. I struggle to see any outcome for the company where they fail to meet their obligations to their Preferred shareholders. If you think the common shares give you too much exposure to Bitcoin price risk then the Preferreds seem like a no-brainer.

The company’s common shares are priced multiples lower than every other publicly traded Bitcoin miner, on every metric. On an EV/Operating Earnings basis, on an EV/Hashrate basis, on an EV/Future Hashrate basis, on a forward PE basis… No matter which way you quantify it, this company is cheap. Like, cyclical commodity producer cheap. Like, I have been absolutely thrilled to own small Australian coal producers during the middle of Chinese bans on coal imports at higher prices than this. Part of why I’m sharing this idea is because when I ran the numbers on SLNH I didn’t believe it and I want more eyes on the risk/reward here to tell me I’m wrong.

The full Soluna story

Since most of my readers probably neither know or understand the ins and outs of Bitcoin or the grid, here are the most important bits to understand the risk/reward of SLNH.

Bitcoin

I won’t give a full explanation of Bitcoin here, feel free to read Satoshi’s Whitepaper if you want a more thorough explanation of the value proposition of Bitcoin. Suffice to say, by contributing to the Bitcoin network (‘mining’) participants secure the network by acting as transaction validators and in exchange are rewarded in both network fees and minting new Bitcoin (at least until all of the existing Bitcoin has been mined). For the purposes of assessing the risk/reward of Bitcoin for Soluna, the most important aspects of Bitcoin are the market price and the present mining difficulty. Because the price of Bitcoin is impossible to predict here I will focus only on the mining difficulty.

After every 2016 Bitcoin blocks are mined, the network adjusts the mining difficulty. This usually happens after ~14 days. When there is more processing power contributing to mining those 2016 blocks (a higher ‘hashrate’) the network increases the mining difficulty. When there is less processing power (a lower ‘hashrate’) the network reduces the mining difficulty. This all happens automatically according to a predetermined algorithm, so if we know the future hashrate, we can also predict the future mining difficulty. Well, one of the benefits of so many Bitcoin mining companies going public in the last two years is we now can project the baseline increases in future hashrate by adding up all of their projected hashrate increases.

As of my writing this, the current hashrate currently mining on the Bitcoin network is 189.58 exahash per second. The present mining difficulty is 24,371,874,614,345T, and the mining difficulty is presently projected to increase to 25,352,917,461,610T at the next difficulty adjustment ~5 days from now. This would be a 4.03% difficulty increase. Based on the presently disclosed miner delivery and operations schedules for all publicly traded Bitcoin mining companies, the hashrate contributing to the Bitcoin network will undoubtedly increase (and therefore the difficulty of mining will also increase proportionally) by at least 50% by the end of 2022. In the above spreadsheet RandomInvestor also ads an additional 25 exahash to the projections of the public miners to account for additional private miners coming online this year. I think an additional 25 exahash is actually higher than we will see this year because of present supply chain constraints in semiconductors, but I am very confident that the difficulty will increase by 50% this year. A 50-70% increase in Bitcoin mining difficulty is therefore what we will use for our profitability calculations.

The Grid

The electric grid has a lot of problems, that I won’t go into here (if you want a small taste of the number of problems that the grid has, Meredith Angwin’s book Shorting the Grid is an excellent place to start), but one of the big problems facing the grid is that where energy is being produced isn’t always where that energy can be consumed. This inconvenient fact is behind many of the grid’s most difficult to solve problems. Even when energy is being produced in places with a lot of demand (like large population centers) energy consumption is highly variable. People consume less power at night. They also consume more power when the temperature is high (air conditioning), or when the temperature is low (heating). But often this demand variability doesn’t match up with the variability in available power. If you live in the PNW for example, Bonneville Power Administration (BPA) generates varying amounts of power based primarily on precipitation and snow melt due to their reliance on hydropower.1 Increased snow melt and precipitation have almost nothing to do with the power consumption habits of residents of Portland or Olympia. So what happens to all of the excess power generated during the times when people are sleeping, or when snow melts cause the Columbia River to flow higher than normal for weeks at a time? That’s called a power ‘oversupply’ and among other things it can cause power outages so what energy producers do instead of oversupplying the grid and letting it fail is what’s called energy ‘curtailment.’ This is especially true for wind and hydropower producers.

Curtailment is what happens when an energy producer is forced to artificially reduce their energy output below what is able to be produced because it’s above what the grid is able to handle. Going back to our BPA example, I’ll quote from a 2013 paper about this problem (emphasis mine):

In the past, this excess hydropower generated during high water flows was less problematic because there was sufficient capacity on the BPA’s transmission system to accommodate the increased generation. However, in recent years, a boom in wind power generation and its subsequent integration onto the BPA’s transmission system has stressed the transmission grid. Thus, there is not sufficient capacity on the transmission system for the excess hydropower generated during high water events, which can last anywhere from a few days to more than a month, and existing wind power connected to the BPA’s system. In order to accommodate the increased hydropower entering the transmission grid, the BPA reduces the amount of wind power it transmits on its system. Otherwise, the BPA claims that it would not be able to satisfy its statutory mandates to maintain transmission reliability, keep costs to its consumers low by not paying for wasted power generation, and comply with regulations protecting endangered fish species. To satisfy these obligations, the BPA implemented its Environmental Redispatch and Negative Pricing Policy (Redispatch Policy) in 2011, which mandated that other sources of energy connected to the BPA’s transmission system be shut down when excess hydropower was generated.

This is happening all over the world right now. Due to a plethora of robust subsidies, tax incentives (the US Energy Policy Act of 2005 providing $2.7 billion for renewable production credits is a great example), and renewable energy mandates, renewable power sources are being added to the grid by the truckload. Because these sources of power are generating variable rates of power (the wind doesn’t blow at a constant speed, the amount of sun hitting solar panels isn’t constant, and we’ve already talked about hydro) they often are producing too much power at the same time. This has both made the grid exponentially more fragile than it used to be, and resulted in a lot of energy curtailment. And that curtailment is expensive. Setting aside the mechanical and environmental costs of curtailment which are too complex to talk about here, curtailment often comes with significant legal costs.

In 2011 BPA lost a lawsuit from wind energy producers because it was determined that they were preferentially curtailing wind energy over hydro during times of energy oversupply. The Washington Utilities and Transportation Commission hasn’t been happy with BPA’s curtailment either. In 2006 Washington voters passed the Energy Independence Act which mandated that by 2020 15% of all energy production in the state of Washington come from a basket of renewable sources. By cutting wind energy production outputs BPA is effectively reducing the amount of consumable renewable energy available in the Washington grid, making reaching 15% more difficult. Curtailment also means that energy producers miss out on those afforementioned renewable energy subsidies and tax credits.

Soluna’s Value Proposition

SLNH’s primary value proposition is to eliminate the need for energy curtailment. No more wasted energy, no more stress on the grid. SLNH will buy every megawatt of available power from renewable sources. This means higher profit margins for green energy producers, and a more stable and reliable grid for consumers. No more worrying about curtailment lawsuits, no more pressure from states unhappy with less available green energy, and depending on the jurisdiction you might even get access to some additional subsidies or tax credits as a bonus.

Their secondary value proposition is to the Bitcoin network, where their computing power is currently being deployed to secure the network and validate transactions.

The third value proposition is in the not-too-distant future when SLNH will begin selling their green computing power as a product for applications like machine-learning, AI, and scientific computing. Because of SLNH’s absurdly low energy costs, I suspect that their margins for this product (or suite of products) will be the best in the business. If I were leading the SLNH software team my first priority would be to create a green computing product that could be sold to Big Tech. Amazon, Alphabet, Meta, and Disney would be very high on my list of ideal customers and I strongly suspect based on things that both John Belizaire and the Soluna Computing CTO, Dipul Patel, have said that this is the direction the company is currently headed. But for now, that’s pure speculation and should be taken with less than a grain of salt.

The Numbers

I won’t speculate on the company’s margins for selling a green computing product which doesn’t yet exist, nor will I pretend to know when that will aspect of the business will materialize (though they have repeatedly said we will catch a peak at it this year). Instead, let’s look at what’s already here and what’s most likely to materialize this year.

As of December 9th, SLNH had ~50MW of mining equipment fully energized and deployed contributing 623 petahash (0.623 exahash) worth of mining power to the Bitcoin network, making up 0.329% of the current hashrate of the network. The company currently expects to have over 1 exahash of mining power active by the end of Q1 of this year. If we simply ignored the company’s planned expansions and annualized their November revenues, the company would generate $23.3 million in FCF in 2022, which already gives them a forward PE under 7.2 (These numbers are coming straight from their December 9th update, I’m not just pulling numbers out of thin air.) If instead we assume that the company expands to their planned 1 exahash by the end of March and then stops there, assuming November’s Bitcoin mining profitability numbers and annualizing their forcasted March earnings at present Bitcoin difficulty rates and ~$45,000 Bitcoin gives them an annualized earnings of over $40 million and a forward PE of ~4. But obviously, they’re not going to stop building out the business in March. Additionally, let’s not forget that the price of Bitcoin has dropped since these estimates, and the mining difficulty of Bitcoin is probably going to go up by at least 50% this year. So let’s get more realistic.

Soluna monetizes their Bitcoin mining assets in two ways: Hosting, and Mining. Hosting refers to splitting the revenue of Bitcoin mining equipment with another entity while SLNH retains the ownership rights of the equipment. Mining is just that but without sharing the revenue, so SLNH retains all of the profits. As you’d expect, Hosting generates half of the profits that their Mining does: ~35% profit margins for hosting, and ~70% margins for Mining. Presently, the company is operating at about a 30/70 Hosting/Mining split and has given every indication that this will continue for the foreseeable future. This means that about 15% of the company’s future profits will come from Hosting, and 85% will come from Mining, making the company’s net profit margins ~65%. But these are December numbers when the mining difficulty was lower and the price of Bitcoin was higher, much higher.

If we accept the company’s numbers of $210 in revenue per petahash per second as of December 9th, how does the price of Bitcoin and the network’s mining difficulty compare to then? Let’s say the average price of Bitcoin in November was $60,000. As of today the price is ~$43,000 but let’s call it $40,000 for simplicity’s sake. Assuming that the mining difficulty since then has remained constant that brings their earnings down from $210/petahash/second to $140/petahash/second. If we multiply that by their hashrate as of December 9th of 623 that gives us an earnings of $75,358.08 per day, or $27,505,699.20 per year.

Now, to deal with that pesky periodically increasing mining difficulty… Instead of doing the work of adjusting each month’s earnings based on a projected network difficulty increase every two weeks, let’s make this absurdly simple. Let’s assume that today the mining difficulty has already reached wherever we think it will end up by the end of the year. I think 50% is a conservative number even the most bullish case has to assume, and 70% seems a little unrealistic but is still possible. So let’s say that it’s 70% to give ourselves a margin of safety. Assuming we believe the company’s estimate of bringing online 233MW of mining power this year, and we assume they’re using older mining equipment (supply chains aren’t about to magically manifest the latest and greatest after all) that will bring them up to ~4 exahash per second by the end of 2022.

Assuming that the Bitcoin network difficulty and hashrate increases by 70% from it’s current 189.58 exahash, that implies a Bitcoin network hashrate of 322.286 exahash. Which, given the company’s planned 4 exahash brings them up from 0.329% of the Bitcoin network to 1.241% of the network. Which means even with the difficulty increases they will still expand their net take home of Bitcoin by several times. Annualizing our revenue rate of $140/petahash/second gives us a new annualized revenue of $176,601,600, nothing to scoff at for a ~$150 million marketcap company. Even if we give their profit margins a healthy haircut from 65% down to 50% due to the increased mining difficulty that still gives us a December 2022 annualized EPS of $6.04/share which is a forward PE of just over 1.785.

If we give both their earnings and the profit margins another 20% haircut (let’s say not only does the Bitcoin mining difficulty goes up more than 70%, but the price of Bitcoin continues to drop significantly as well) we still end up at an annualized December forward EPS of $3.87/share and a forward PE of 2.79.

This is the most bearish case I can see for the company, without introducing some kind of a catastrophic failure at one of their sites that seems like such an improbable left tail risk that it barely merits consideration. If we don’t assume that everything that could conceivably go wrong will go wrong and instead accept SLNH’s own projections (which have historically been conservative), the company currently trades for a forward PE of <1 and will continue to expand their revenues exponentially for the foreseeable future. Given what I think is likely to be 2-3 years of exponential growth for them, I would be thrilled to buy SLNH shares if they had a marketcap of $600 million right now, and I am honestly befuddled that they aren’t.

The Conclusion

By using Bitcoin to increase grid reliability and make renewable energy viable SLNH finds themselves at the intersection of a lot of right tail factors that will likely carry them (and their stock price) for the foreseeable future. I happen to personally think that ‘renewable energy’ is a meme that has been disasterous for the grid, but SLNH solves one of renewable energy’s biggest problems. The sheer number of ‘green’ investment funds these days is staggering and I would be shocked if SLNH isn’t soon included in many of them (for example, Changebridge Capital added SLNH to their holdings in November). Heck, their currently in development green cloud computing suite could’ve easily been a $150 million SPAC on its own this year. For me, there is simply too much about this company that could go right that I’m willing to accept the risk of owning a tech stock, even one that gives me Bitcoin price risk in a higher interest rate environment. If that still seems like too much risk for you, then the company’s preferred shares seem like a way to collect a very high yield with very little downside.

Disclosure: I have a beneficial long position in the shares of SLNH through both stock ownership and options. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with Soluna and merely stumbled across them because I have a curiosity with the Bitcoin mining space and have been following the company since early last year.

Drew Pearsall, Notes and Comments, The Bonneville Power Administration's Energy Curtailment Problem: An Analysis of Its Redispatch Policy and Oversupply Protocol P and Their Impact on Washington's Wind Power Producers, Utility Companies, and Energy Independence Act, 3 Wash. J. Envtl. L. & Pol'y 79 (2013). Available at: https://digitalcommons.law.uw.edu/wjelp/vol3/iss1/4

Great article Astrid! Today I was learning about Hashrate and difficulty. Super useful. Would just add the analogy that, at 2.3 cents/KWh, these projects are like being able to extract Oil in Saudi Arabia. No matter the bitcoin price drop or the increase in difficulty, they will still accumulate cash